I acknowledge the Gadigal people, traditional custodians of the land on which we gather today, and pay my respects to their Elders past and present.

I’d also like to acknowledge the Sydney Institute and its long‑standing commitment to encouraging big conversations about big issues.

Introduction

In 2012, I spoke here about why inequality matters, and what we should do about it (Leigh 2012).

Returning a decade later, I’m even more convinced that market power is a critical part of Australia’s economic story.

It’s hard to ignore the growing body of evidence that suggests excessive market concentration can lead to economic problems.

Dominant firms in a market may have less incentive to carry out research and development.

They may have less incentive to produce new products.

And in some cases, they may have less incentive to pay their employees fairly.

As you can imagine, the drag on the economy only becomes stronger and deeper with each and every concentrated market.

The challenge for economists is to better understand the problems and that means measuring them.

Markups — the gap between production cost and selling price — are one of the most reliable indicators of market power.

Drawing on new evidence, today I’d like to present analysis on what markups can tell us about competitiveness in Australia.

The concentration game

Concerns about market power are not new.

In fact, most people have a pretty good idea about these concepts thanks in part to Lizzie Magie.

If your 9‑year‑old has bankrupted you playing Monopoly then you would be familiar with her work.

Magie grew up in the aftermath of the Civil War when the ‘Robber Barons’ controlled much of the American economy.

It was an era where monopolists such as Cornelius Vanderbilt, John D. Rockefeller, and Andrew Carnegie loomed large.

As the story goes, Magie’s father introduced her to the ideas of economist Henry George.

George sought to explain how extreme wealth could exist alongside deep poverty in 19th century cities.

He argued that the monopoly ownership of land was to blame and proposed a land tax to lessen landowners’ ability to extract wealth from renters.

George’s ideas struck a chord with Magie and she created The Landlord’s Game, the very first version of Monopoly.

She designed the boardgame to serve as an interactive critique of monopoly power.

Her motive was clear: show players how land grabbing enriched property owners and impoverished tenants.

In planting a seed for generations to come, Magie wrote:

Let the children once see clearly the gross injustice of our present land system and when they grow up, if they are allowed to develop naturally, the evil will soon be remedied.

During the Great Depression — and following the removal of Magie’s radical overtones — Monopoly became a best seller for the Parker Brothers.

In fact, the Parker Brothers had to pay Magie off after she protested that her patent had been ripped off.

She was paid $500 but never really acknowledged as the game’s creator.

Another glaring inequity.

Measuring market power

Concerns about market power have been around for a while but in the past decade we’ve seen a huge increase in the number of studies.

Let me catch you up on the measures and the methods as well as the flaws and findings.

The measures

Concentration is the most frequent measure of market power because it only requires information on firm revenues.

For example, my previous research with Adam Triggs (Leigh and Triggs 2016) used IBIS World data to estimate market concentration.

Market concentration tells us how much share the biggest players have. But it doesn’t tell us the extent to which they’re throwing their weight around.

By contrast, markups – the gap between firms’ costs and what they charge their consumers – go more directly to the impact on consumers.

In that sense, markups are capturing the market power of firms: their ability to influence the price at which they sell their products.

It’s easiest to see this at the extremes. With thousands of companies selling a similar product, there’s a going price, and that’s what sellers charge. The market sets the price. By contrast, when only one company sells the product, they set the market price.

The difference is between market pricing and monopolist pricing.

The methods

We know markups are a useful measure, but the challenge is getting the right data to measure them accurately. Ideally, economists would like to know each firm’s marginal costs. Unsurprisingly, most companies do not publish this information on their websites.

To get around this problem, economists have developed various ways to estimate markups.

Robert Hall (1988) was the first to propose a method using accounting data and the assumption that firms minimise their costs to estimate markups.

From 2012 onwards, Belgian economist Jan De Loecker and his co‑authors extended the Hall (1988) method.

They show how combining estimates of ‘production functions’ – the way firms produce output from labour, capital, and ‘intermediate’ inputs – with the cost minimisation assumption can provide us with estimates of markups.

Their work led to an explosion of research into markups across the world.

The flaws

But there are some critics.

Both Susanto Basu (2019) and Steve Bond and co‑authors (2020) argue that some of the startling findings of steeply rising markups are difficult to reconcile.

They say for the results to be interpreted as equal to markups on prices over marginal costs, firms must not have market power over the inputs they use in production.

For example, they point out that big firms may have the ability to influence the price they pay for labour – what Cambridge economist Joan Robinson dubbed ‘monopsony power’.

In response, De Loecker and co‑authors agree that their estimates might be biased by firms’ market power over input markets.

However, they say that in these instances the markup estimates are also measuring firms’ market power over the factors of production that they use.

Basu (2019) also argues that the ‘rising markups’ story doesn’t fit the fact that the 2000s and 2010s saw a tight US labour market and subdued inflation. The problem with this critique is that so many other factors influence employment and prices over this period, including a global savings glut, China’s economic rise and monetary policy. Perhaps prices would indeed have been lower if markups had not risen.

Other macroeconomic trends support the theory of increasing markups. These include low business investment, high and persistent corporate profits, and a declining labour share of income.

Ultimately, despite some concerns about the data used, the De Loecker method of estimating markups provides reasonable evidence that helps explain some significant patterns in the data.

The findings

Researchers have used the De Loecker method to estimate markups in the US and across the world.

De Loecker, Eeckhout and Unger (2020) found average markups in the US increased from 21 per cent above marginal cost in 1980 to 61 per cent above marginal cost in 2016.

The authors found that markups increased the most for high‑markup firms and show that this is due to increased market power.

The authors also showed that high‑markup (and highly profitable) firms attracted a greater share of resources, a phenomenon closely linked with the rise of ‘superstar’ firms.

As the name suggests, ‘superstar’ firms are large and have come to dominate their industries. David Autor and co‑authors (2020) showed that those industries with the largest growth in market share going to these ‘superstars’ also saw the steepest decline in the share of income flowing to workers.

Looking further afield, De Loecker and Eeckhout (2018) estimate markups for 70,000 firms in 134 countries between 1980 and 2016.

They found average markups increased globally from around 10 per cent in 1980 to 60 per cent in 2016.

This is driven by firms with already high‑markups seeing the greatest estimated increase – consistent with previous evidence showing growing dispersion of markups.

The International Monetary Fund (2019) also analysed approximately 900,000 firms in 27 countries and found an increase in markups between 2000 and 2015 (though more modest than the rise observed by De Loecker and Eeckhout 2018).

Global evidence supports the increase in markups being partly linked to the rise of superstar firms (though perhaps not as much as in the US), and suggests that an increase in markups is partly responsible for the decline in the labour share of income.

The decline in labour share worldwide seems to be driven primarily by a reallocation of resources to firms with a relatively low labour share of income.

However, the international results from De Loecker and Eeckhout (2018) should be treated with caution.

The dataset used is likely not representative: for example, the sample of Australian firms included from before 2000 will be very narrow.

Also, econometric estimates from US firms are applied to all firms worldwide to calculate markups, which is a strong modelling assumption.

Australian markups and market power

That leads me to analysis of markups in Australia and some observations in 4 significant areas.

How Australia compares

The first area is how Australia compares to other advanced economies.

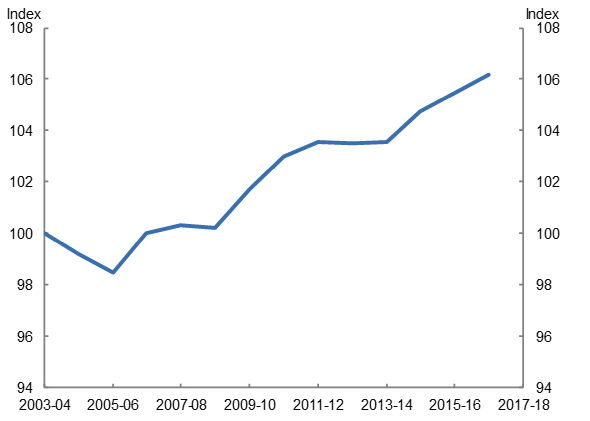

Ground breaking research by Jonathan Hambur (2021) used Australian firm‑level microdata to estimate markups. Taking on board one of the criticisms made of the markups estimation literature, he focuses on the change in markups, not the level of markups.

Hambur’s findings – reproduced in Figure 1 – suggest industry average markups increased by around 6 per cent between 2003 and 2016: slightly below the average for advanced economies estimated by the IMF over the same period.

Interestingly, firms in the top 10 per cent of the distribution of markups have, on average, the highest market share.

However, unlike in the US, there is no evidence of reallocation of resources towards high markup firms.

Figure 1: Average firm level mark ups in Australia

Notes: Index = 100 in 2003‑04; unweighted.

Source: Hambur (2021)

Technology and markups

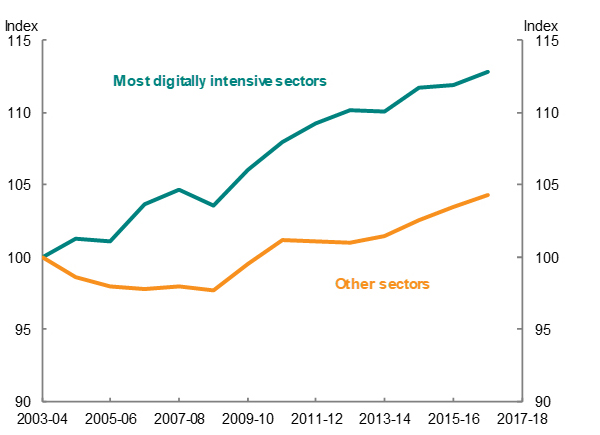

The second area of great interest is technology.

Changing technology may explain higher firm concentration and markups.

Software and other digital technologies often have increasing returns to scale — meaning outputs grow faster than inputs.

This inherently offers greater benefits to larger firms.

This is particularly true for digital firms that have very low marginal costs and operate in markets with strong network effects.

As Figure 2 shows, between 2003 and 2016, markups for the most digitally intensive firms increased by 12 per cent, compared with 4 per cent for all other firms.

Figure 2: Markups by digital intensity of industry

Notes: Index 2003‑04=100. Industries assigned a digital intensity based on the taxonomy outlined in Table 3 of Calvino et al (2018). Requires mapping of ISIC classifications used in that paper, to the ANZSIC classifications used in BLADE. Firm‑weighted averages then taken for each quartile of industries. Most digitally intensive sectors are top quartile. All other sectors are an unweighted average of the series for the other three quartiles.

Source: Hambur (2021)

These results suggest that changing technology played a role in increasing markups.

However, markups have also increased for less digitally intensive firms, suggesting other dynamics, like an increase in market power, are also important.

Other factors and markups

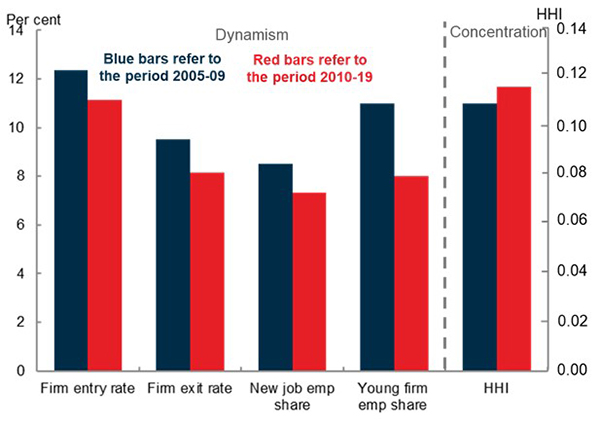

The third observation is of how the findings on markups relate to the broader challenges facing our economy.

The evidence from markups aligns with other evidence suggesting competitive pressure in the economy has declined.

As Figure 3 shows, the period from 2005‑09 to 2010‑19 saw a decline in market dynamism across a host of measures.

Firm entry and exit rates have declined.

There’s a lower share of employees working at young firms.

Job mobility has declined.

At the same time, the largest firms have increased their market share, as shown by the rise in the Herfindahl index of market concentration.

Figure 3: Dynamism and concentration measures

Notes: Entry and exit rates are for employing firms. Young firm employment share calculated by e61 over slightly different time periods (2000s and 2010+). HHI is the sum of squared market shares of all firms in each industry. The HHI ranges between 0 and 1, with smaller scores reflecting less concentrated markets.

Sources: ABS Counts of Australian Businesses, including Entries and Exits; ABS Labour Force microdata; e61.

Industry‑level changes

Declining dynamism in the product and labour markets have occurred simultaneously.

There is also some evidence of a correlation across sectors. For example, job mobility rates have dropped more in those sectors where the share of young firms has seen the largest declines (Adams et al 2022).

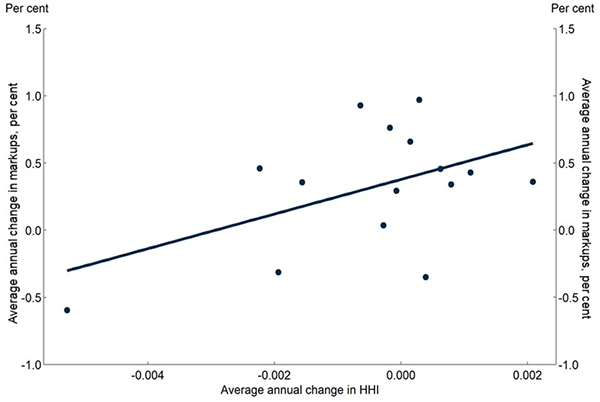

What about when it comes to market concentration and markups?

In Figure 4, we plot industry‑level changes in concentration on the horizontal axis against industry‑level changes in markups on the vertical axis. This allows us to see whether the industries that become more concentrated also see bigger increases in markups.

The fitted line in Figure 4 shows an upwards slope, indicating that between 2003 and 2016 the industries that saw the greater consistent annual increase in concentration saw, on average, greater annual increases in markups.

The fitted line is statistically significant at the 10 per cent level, with a slope of 1.29.

This is suggesting that an increase in the growth rate of the Herfindahl index by 0.001 is associated with an increase in the growth rate of markups of 0.129 percentage points.

We should not make too much of a result that holds at only the 10 per cent level. Perhaps the best way to regard it is that it provides suggestive evidence of a link between the growth in markups and growth in market concentration.

Figure 4: HHI and markups by industry

Notes: Average annual growth rates calculated from 2003‑04 to 2016‑17. HHI is the sum of squared market shares of all firms in each industry. The HHI can range between 0 and 1, with smaller scores reflecting less concentrated markets.

Source: Treasury calculations based on ABS BLADE data.

This finding is consistent with new research from thinktank E61, suggesting that more dynamic markets would benefit most workers (Adams et al 2022).

This is partly because higher rates of new firm creation and labour mobility increase the value of workers’ outside options.

Adams et al (2022) also show that the pass‑through of productivity to wages – the extent to which workers benefit from greater productivity – has fallen most in industries that saw the steepest declines in entry rates.

Before I wrap up, let me acknowledge the Treasury officials for both the research drawn on in this presentation and more broadly.

Treasury has published papers on Australia’s productivity challenges in the latest edition of the department’s in‑house journal, Economic Roundup. This work, by Zac Duretto, Omer Majeed, Jonathan Hambur, Iris Day, and Patrick Hartigan, draws heavily on the impressive data‑crunching ability of the Australian Treasury. Outside central banks, it is rare to have a government agency that is producing so much cutting‑edge research. This is a credit to Treasury Secretary Dr Steven Kennedy, and his willingness to invest in the infrastructure and personnel who have led the work in this critical area.

Closing remarks

Studying markups can tell us a lot about the competitiveness of our economy.

Like other advanced nations, markups in Australia have increased since the turn of the century. Australia’s most digitally intensive firms increased markups the most.

Australian industries with the greatest increase in concentration also recorded the greatest increases in markups.

This aligns with other economic evidence around declining dynamism.

But I’m optimistic about the path ahead.

It’s not easy.

Unlike when you’re playing Lizzie Magie’s Monopoly, there is no get‑out‑of‑jail‑free card. There’s no Chance card that will let us suddenly advance to Go and collect $200.

But Australia has an opportunity to boost productivity — the key to increasing living standards.

It’s terrific to see a renewed focus on productivity from people across the community from policymakers to researchers to business leaders.

The Jobs and Skills Summit sparked many of these conversations, and productivity and wages will feature in the Employment White Paper to follow.

In the meantime, I welcome debate on markups — the malign markers for the Australian macroeconomy.

And I look forward to returning to the Sydney Institute in 2032 to discuss what I hope will be a more dynamic and competitive Australian economy.

References:

Adams, N., et al., 2022. “Better harnessing Australia’s talent: five facts for the Summit”, e61 Institute, Sydney.

Arablouei, R. and Abdelfatah, R., 2022. “'Throughline': There's more to the board game Monopoly than you might think”. NPR Morning Edition, 27 July 2022.

Basu, S., 2019. "Are Price‑Cost Markups Rising in the United States? A Discussion of the Evidence." Journal of Economic Perspectives, Vol. 33, No. 3, 3‑22.

De Loecker, J., and Eeckhout, J., 2018. “Global Market Power”, National Bureau of Economic Research Working Paper 24768.

De Loecker, J., Eeckhout, J., and Unger, G., 2020. “The Rise of Market Power and the Macroeconomic Implications”, The Quarterly Journal of Economics, Volume 135, Issue 2, 561‑644.

Hall, Robert E., 1988. “The Relation between Price and Marginal Cost in U.S. Industry,” Journal of Political Economy, 96 (5), 921–947.

Hambur, J., 2021 “Product Market Power and its Implications for the Australian Economy”, Treasury Working Paper 2021‑03, June 2021.

Leigh, A. and Triggs, A., 2016. “Markets, Monopolies and Moguls: The Relationship between Inequality and Competition”, Australian Economic Review, vol. 49, issue 4, 389‑412.

Leigh, A., 2012. “Why Inequality Matters, and What We Should Do About It”, Speech to the Sydney Institute, Sydney, 1 May 2012.

Leigh, A., 2022. “A More Dynamic Economy”, FH Gruen Lecture, Australian National University, Canberra, 25 August 2022.

Magie, L., 1902. "The Landlord's Game", The Single Tax Review, Autumn 1902, 56.

Syverson, C., 2019. “Macroeconomics and Market Power”, The Journal of Economic Perspectives, Vol. 33, No. 3, 23‑43.